The actual dashboard.

No mockups — this is the real tool you run on your own machine. Click any shot to enlarge.

Backtest on real market data — scored against just holding.

Real OHLCV from 6 exchanges + forex. Realistic fees & slippage, full risk controls (position size, risk-per-trade, ATR / swing stops, trailing). Every result is measured against a Buy & Hold line — so you see the honest truth, not a cherry-picked number.

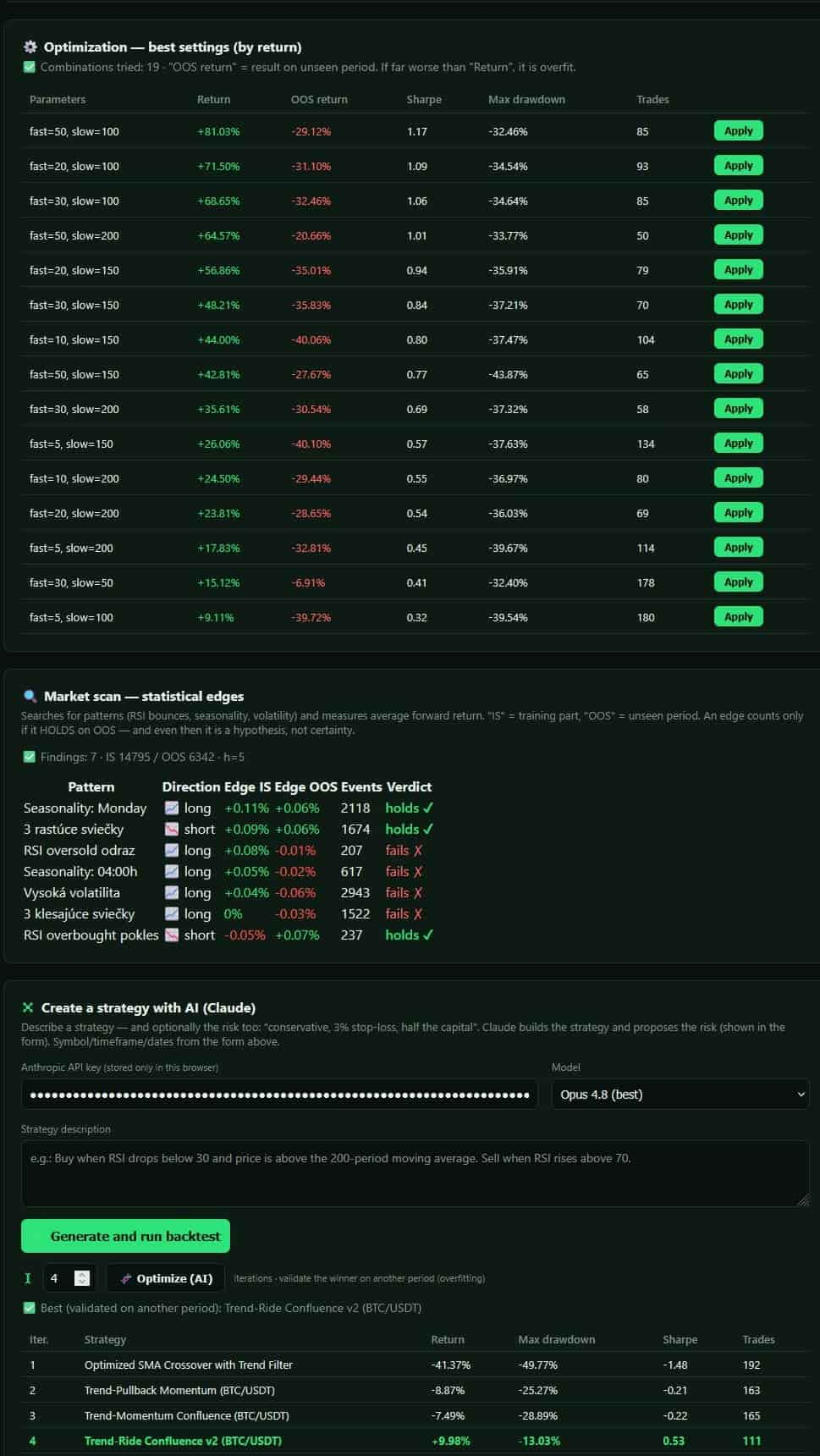

Tune it — then survive the unseen data.

Grid-search tunes parameters and risk, then validates the winner out-of-sample. The red OOS column exposes overfitting at a glance. The market scan hunts statistical edges (RSI bounces, seasonality, volatility) and labels each "holds ✓" or "fails ✗" on unseen data.

AI builds a strategy as a safe, structured spec.

Describe a strategy in plain words; Claude returns a structured JSON spec (indicators, entry/exit, risk) — no raw code ever runs, so it's safe to share. The self-evolving loop iterates and honestly reports when a winner does NOT hold out-of-sample.